|

|

|

|

|

|

|

|

|

|

Financial Report

|

|

Independent Auditor’s Report

Independent auditor’s report to Hong Kong Council for Accreditation of Academic and Vocational Qualifications (Established under the Hong Kong Council for Accreditation of Academic and Vocational Qualifications Ordinance) We have audited the financial statements of Hong Kong Council for Accreditation of Academic and Vocational Qualifications (the “Council”) set out on pages 58 to 89, which comprise the balance sheet as at 31 March 2011, statement of comprehensive income, statement of changes in reserves and cash flow statement for the year then ended and a summary of significant accounting policies and other explanatory information. The Council’s responsibility for the financial statements The Council is responsible for the preparation of financial statements that give a true and fair view in accordance with Hong Kong Financial Reporting Standards issued by the Hong Kong Institute of Certified Public Accountants and for such internal control as the Council determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s responsibility Our responsibility is to express an opinion on these financial statements based on our audit. This report is made solely to you, as a body, in accordance with section 15 of the Hong Kong Council for Accreditation of Academic and Vocational Qualifications Ordinance (Cap.1150), and for no other purpose. We do not assume responsibility towards or accept liability to any other person for the contents of this report. We conducted our audit in accordance with Hong Kong Standards on Auditing issued by the Hong Kong Institute of Certified Public Accountants. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of the financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Council, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements give a true and fair view of the state of affairs of the Council as at 31 March 2011 and of its surplus and cash flows for the year then ended in accordance with Hong Kong Financial Reporting Standards. KPMG Certified Public Accountants 8th Floor, Prince’s Building 10 Chater Road Central, Hong Kong 25 August 2011 Statement of comprehensive income for the year ended 31 March 2011 (Expressed in Hong Kong dollars)

Balance sheet as at 31 March 2011 (Expressed in Hong Kong dollars)

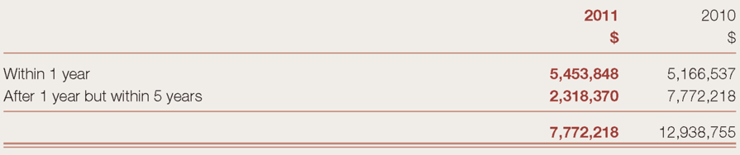

Approved and authorised for issue by the Council on 25 August 2011 |

Chairman |

Executive Director

Executive Director

|

||

|

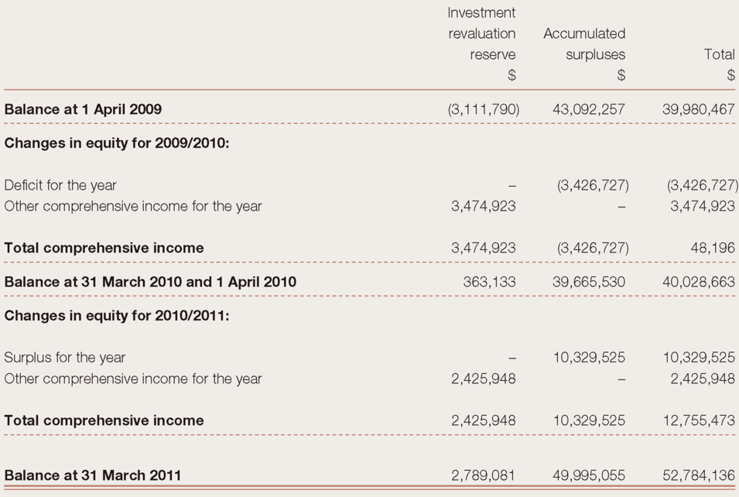

Statement of changes in reserves for the year ended 31 March 2011 (Expressed in Hong Kong dollars)

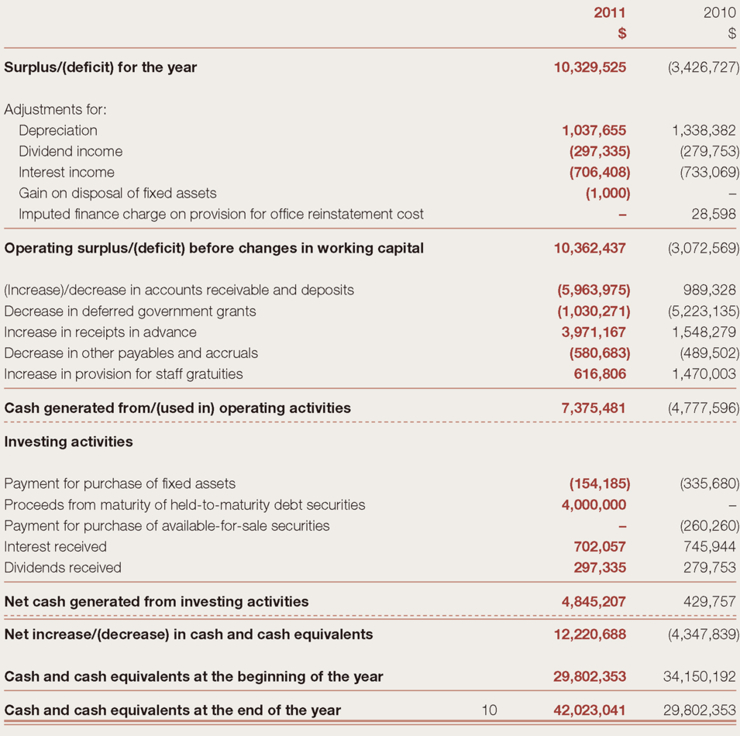

Cash flow statement for the year ended 31 March 2011 (Expressed in Hong Kong dollars)

Notes to the financial statements (Expressed in Hong Kong dollars) 1. Status of the Council Hong Kong Council for Accreditation of Academic and Vocational Qualifications (the “Council”) is a body corporate established under the Hong Kong Council for Accreditation of Academic and Vocational Qualifications Ordinance. Under the Accreditation of Academic and Vocational Qualifications Ordinance (Cap. 592) (the “Ordinance”) the Council assumes its statutory role as the Accreditation Authority and QR Authority under the Qualifications Framework (“QF”). As the Accreditation Authority, the Council is responsible for developing and implementing the standards and mechanisms for accreditation of academic and vocational qualifications to underpin the QF and for organising the accreditation exercises for the purposes as specified in the Ordinance. The Council also provides advice to the Government of the Hong Kong Special Administrative Region on the registration of non-local academic and professional courses, the assessment on nonlocal qualifications and also on educational standards and qualifications generally. Since the Council is not profit-oriented and is not subject to any externally imposed capital requirements, its primary financial and capital management objectives are to maintain a balance between annual income and expenditure, so that it has the ability to operate as a going concern and perform its statutory roles and functions. The Council is primarily financed through the charging of fees for academic and vocational accreditation services rendered which include validations, revalidations, institutional reviews, qualifications assessments and advisory/consultancy services. Any operating surplus shall be carried forward to the following financial year to meet future expenditure required for the operations of the Council. 2. Significant accounting policies (a) Statement of compliance These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting Standards (“HKFRSs”), which collective term includes all applicable individual Hong Kong Financial Reporting Standards, Hong Kong Accounting Standards (“HKASs”) and Interpretations issued by the Hong Kong Institute of Certified Public Accountants (“HKICPA”) and accounting principles generally accepted in Hong Kong. A summary of the significant accounting policies adopted by the Council is set out below. The HKICPA has issued two revised HKFRSs, a number of amendments to HKFRSs and two new Interpretations that are first effective for the current accounting period of the Council. However, none of these developments are relevant to the Council’s financial statements for the years ended 31 March 2010 and 2011. The Council has not applied any new standard or interpretation that is not yet effective for the current accounting period (note 19). (b) Basis of preparation of the financial statements The measurement basis used in the preparation of the financial statements is the historical cost basis except that the investments in equity securities are stated at fair value as explained in the accounting policies set out below. The preparation of financial statements in conformity with HKFRSs requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements about carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of the revision and future periods if the revision affects both current and future periods. Judgement made by the Council in the application of HKFRSs that have significant effect on the financial statements is discussed in note 18. (c) Investments in debt and equity securities The Council’s policies for investments in debt and equity securities are as follows: (i) Investments in securities held for trading are classified as current assets and are initially stated at fair value. At each balance sheet date the fair value is remeasured, with any resultant gain or loss being recognised in surplus or deficit. The net gain or loss recognised in surplus or deficit does not include any dividends earned on these investments as these are recognised in accordance with the policy set out in note 2(l)(vii). (ii) Dated debt securities that the Council have the positive ability and intention to hold to maturity are classified as held-to-maturity securities. Held-to-maturity securities are initially recognised in the balance sheet at fair value plus transaction costs. Subsequently, they are stated in the balance sheet at amortised cost less impairment losses (see note 2(e)). (iii) Other investments in equity securities are classified as available-for-sale securities and are initially recognised at fair value plus transaction costs. At each balance sheet date the fair value of the securities is remeasured, with any resultant gain or loss being recognised directly in other comprehensive income. Dividend income from these investments is recognised in surplus or deficit in accordance with policy set out in note 2(l)(vii). When these investments are derecognised or impaired (see note 2(e)), the cumulative gain or loss is reclassified from investment revaluation reserve to surplus or deficit. (iv) Investments are recognised/derecognised on the date the Council commits to purchase/sell the investments or they expire. (d) Fixed assets Fixed assets are stated in the balance sheet at cost less accumulated depreciation and impairment losses (see note 2(e)). Depreciation is calculated to write off the cost of items of fixed assets, less their estimated residual value, if any, using the straight line method over their estimated useful lives as follows:

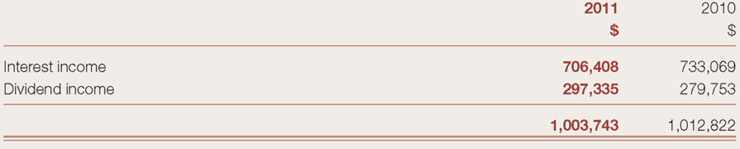

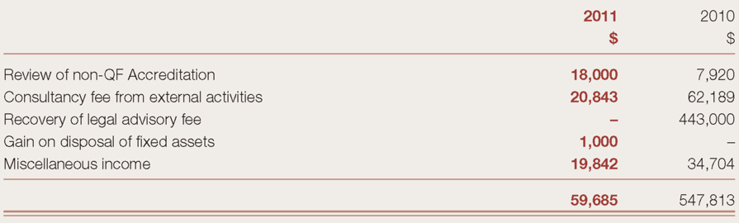

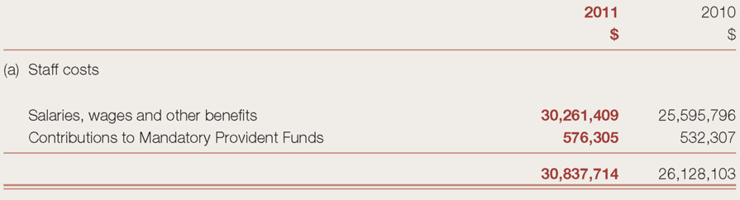

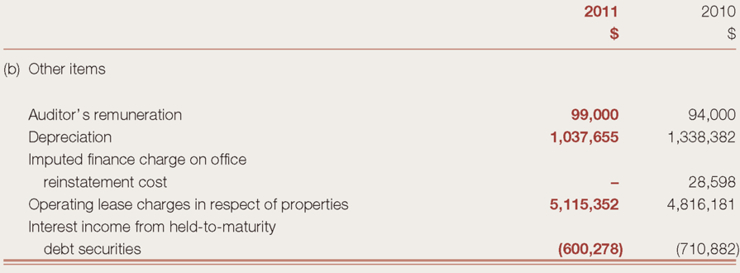

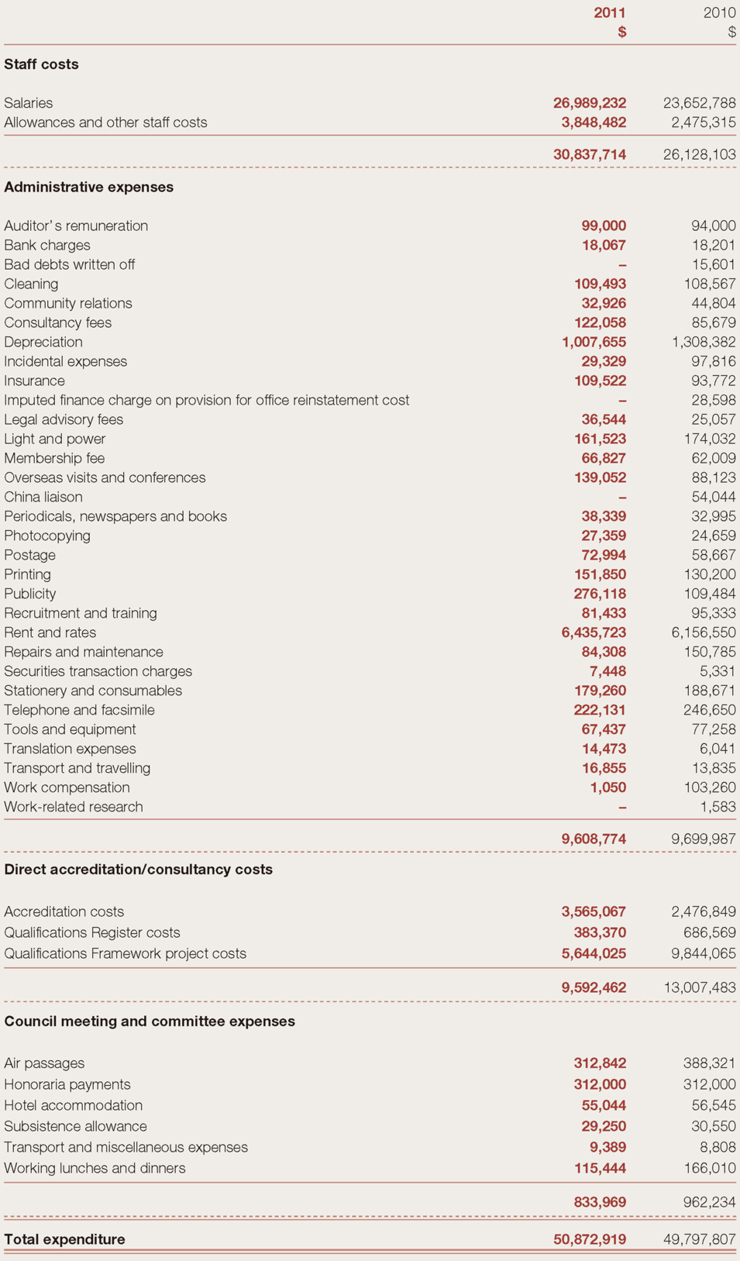

Both the useful life of an asset and its residual value, if any, are reviewed annually. Gains or losses arising from the retirement or disposal of an item of fixed assets are determined as the difference between the net disposal proceeds and the carrying amount of the item and are recognised in the surplus or deficit on the date of retirement or disposal. (e) Impairment of assets (i) Impairment of investments in debt and equity securities and receivables Investments in debt and equity securities and receivables that are stated at cost or amortised cost or are classified as available-for-sale securities are reviewed at each balance sheet date to determine whether there is objective evidence of impairment. Objective evidence of impairment includes observable data that comes to the attention of the Council about one or more of the following loss events: – significant financial difficulty of the debtor; – a breach of contract, such as a default or delinquency in interest or principal payments; – it becoming probable that the debtor will enter bankruptcy or other financial reorganisation; – significant changes in the technological, market economic or legal environment that have an adverse effect on the debtor; and – a significant or prolonged decline in the fair value of an investment in an equity instrument below its cost. If any such evidence exists, any impairment loss is determined and recognised as follows: – For receivables and held-to-maturity debt securities carried at amortised cost, the impairment loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial asset’s original effective interest rate (i.e. the effective interest rate computed at initial recognition of these assets), where the effect of discounting is material. If in a subsequent period the amount of an impairment loss decreases and the decrease can be linked objectively to an event occurring after the impairment loss was recognised, the impairment loss is reversed through surplus or deficit. A reversal of an impairment loss shall not result in the asset’s carrying amount exceeding that which would have been determined had no impairment loss been recognised in prior years. – For available-for-sale equity securities, the cumulative loss that had been recognised directly in investment revaluation reserve is transferred to surplus or deficit. The amount of the cumulative loss that is transferred to in surplus or deficit is the difference between the acquisition cost (net of any principal repayment and amortisation) and current fair value, less any impairment loss on that asset previously recognised in surplus or deficit. Impairment losses recognised in surplus or deficit in respect of available-for-sale equity securities are not reversed through surplus or deficit. Any subsequent increase in the fair value of such assets is recognised directly in other comprehensive income. (ii) Impairment of fixed assets Internal and external sources of information are reviewed at each balance sheet date to identify indications that fixed assets may be impaired or an impairment loss previously recognised no longer exists or may have decreased. If any such indication exists, the asset’s recoverable amount is estimated. An impairment loss is recognised in surplus or deficit if the carrying amount of an asset exceeds its recoverable amount. The recoverable amount of an asset is the greater of its fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of time value of money and the risks specific to the assets. An impairment loss is reversed if there has been a favourable change in the estimates used to determine the recoverable amount. A reversal of impairment losses is limited to the asset’s carrying amount that would have been determined had no impairment loss been recognised in prior years. Reversals of impairment losses are credited to surplus or deficit in the year in which the reversals are recognised. (f) Leased assets Where the Council has the use of assets under operating leases, payments made under the leases are charged to surplus or deficit in equal instalments over the accounting periods covered by the lease term, except where an alternative basis is more representative of the pattern of benefits to be derived from the leased asset. Lease incentives received are recognised in surplus or deficit as an integral part of the aggregate net lease payment made. Contingent rentals are charged to surplus or deficit in the accounting period in which they are incurred. (g) Trade and other receivables Trade and other receivables are initially recognised at fair value and thereafter stated at amortised cost less allowance for impairment of doubtful debts (see note 2(e)), except where the effect of discounting would be immaterial. In such cases, the receivables are stated at cost less allowance for impairment of doubtful debts. (h) Trade and other payables Trade and other payables are initially recognised at fair value and thereafter stated at amortised cost unless the effect of discounting would be immaterial, in which case they are stated at cost. (i) Cash and cash equivalents Cash and cash equivalents comprise cash at bank and on hand, demand deposits with banks and other financial institutions, and short-term, highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value, having been within three months of maturity at acquisition. (j) Employee benefits Salaries, annual bonuses, paid annual leave, contributions to defined contribution retirement plans and the cost of non-monetary benefits are accrued in the year in which the associated services are rendered by employees. Where payment or settlement is deferred and the effect would be material, these amounts are stated at their present values. (k) Provisions and contingent liabilities Provisions are recognised for liabilities of uncertain timing or amount when the Council has a legal or constructive obligation arising as a result of a past event, it is probable that an outflow of economic benefits will be required to settle the obligation and a reliable estimate can be made. Where the time value of money is material, provisions are stated at the present value of the expenditure expected to settle the obligation. Where it is not probable that an outflow of economic benefits will be required, or the amount cannot be estimated reliably, the obligation is disclosed as a contingent liability, unless the probability of outflow of economic benefits is remote. Possible obligations, whose existence will only be confirmed by the occurrence or non-occurrence of one or more future events are also disclosed as contingent liabilities unless the probability of outflow of economic benefits is remote. (l) Income recognition Income is measured at the fair value of the consideration received or receivable. Provided it is probable that the economic benefits will flow to the Council and the income and costs, if applicable, can be measured reliably, income is recognised in the surplus or deficit as follows: (i) fees for rendering of accreditation services to institutions are recognised in the period to the extent the accreditation work is completed; (ii) advisory fees and consultancy fees are recognised in the period in which such services are rendered; (iii) fees for rendering of qualifications assessment services are recognised in the period in which such assessment work is completed; (iv) qualifications registry fees are recognised in the period in which such services are rendered; (v) government grants are recognised in the balance sheet initially as deferred income when there is reasonable assurance that they will be received and that the Council will comply with conditions attached to them. Grants that compensate the Council for expenses incurred are recognised as income in surplus or deficit on a systematic basis in the same periods in which the expenses are incurred; (vi) interest income is recognised as it accrues using the effective interest method; and (vii) dividend income from listed investments is recognised when the share price of the investment goes ex-dividend. (m) Related parties For the purposes of these financial statements, a party is considered to be related to the Council if: (i) the party has the ability, directly or indirectly through one or more intermediaries, to control the Council or exercise significant influence over the Council in making financial and operating policy decisions, or has joint control over the Council; (ii) the Council and the party is subject to common control; (iii) the party is an associate of the Council or a joint venture in which the Council is a venturer; (iv) the party is a member of key management personnel of the Council, or a close family member of such an individual, or is an entity under the control, joint control or significant influence of such individuals; (v) the party is a close family member of a party referred to in (i) or is an entity under the control, joint control or significant influence of such individuals; or (vi) the party is a post-employment benefit plan which is for the benefit of employees of the Council or of any entity that is a related party of the Council. Close family members of an individual are those family members who may be expected to influence, or be influenced by, that individual in their dealings with the entity. 3 Investment income  4 Other income  5 Surplus/(deficit) for the year Surplus/(deficit) for the year is arrived at after charging/(crediting):

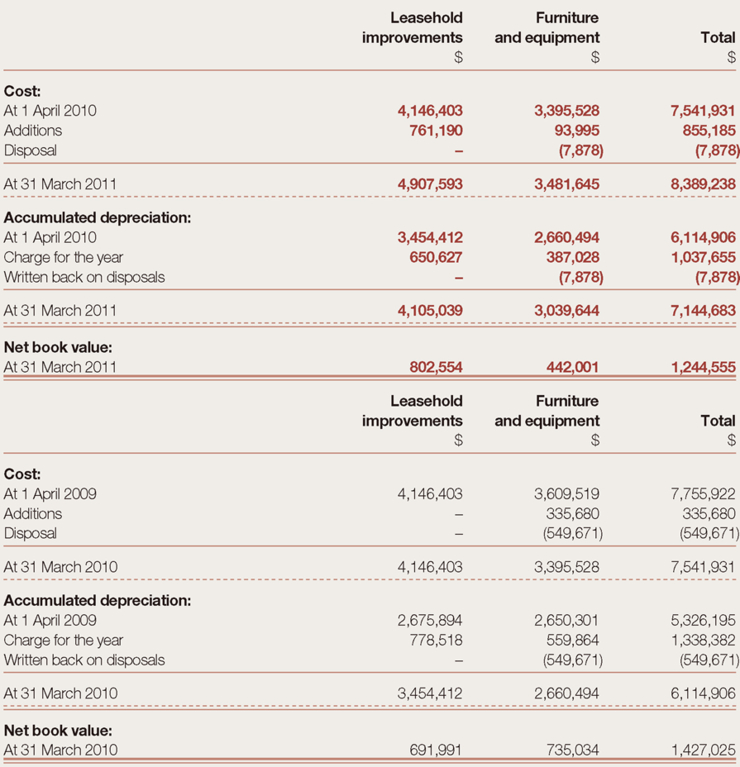

The above staff costs do not include salaries, wages and other benefits of $4,575,483 (2010: $7,663,812) and contributions to Mandatory Provident Funds of $124,429 (2010: $132,161) relating to the Qualifications Framework project which are included in direct accreditation/consultancy costs in the statement of comprehensive income.  6 Taxation No provision for Hong Kong profits tax is required to be made in these financial statements as the Council is exempted from taxation pursuant to section 87 of the Inland Revenue Ordinance. 7 Fixed assets

Included within the cost of leasehold improvements is estimated cost of $1,876,485 (2010: $1,176,485) relating to office reinstatement. 8 Investments

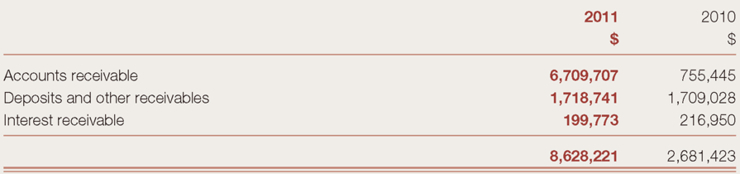

9 Accounts receivable and deposits  All of the accounts receivable and deposits, apart from rental

and utility deposits of $1,670,371 (2010: $1,672,171), are

expected to be recovered within one year.

All of the accounts receivable and deposits, apart from rental

and utility deposits of $1,670,371 (2010: $1,672,171), are

expected to be recovered within one year.

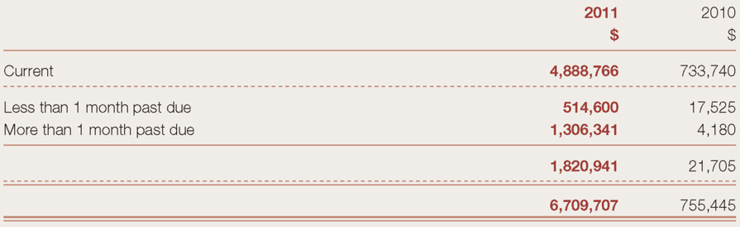

Accounts receivables are due on presentation of billings. Further details on the Council’s credit policy is set out in note 15(a). The ageing analysis of accounts receivable is as follows:

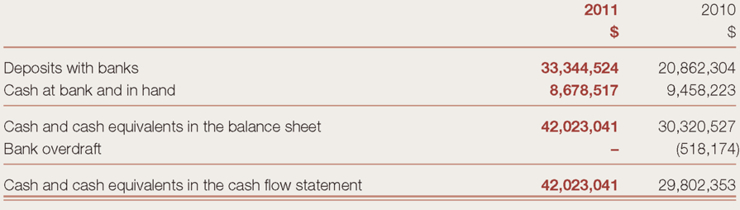

All of the Council’s accounts receivable are not impaired as at 31 March 2011 and 2010. Based on past experience, management believes that no impairment allowance is necessary in respect of these balances as there was no recent history of default and there has not been a significant change in credit quality of the customers. The Council does not hold any collateral over these balances. 10 Cash and cash equivalents

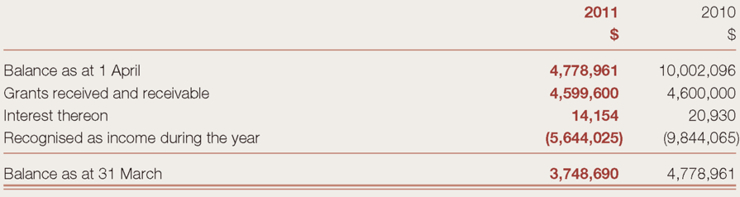

11 Deferred government grants

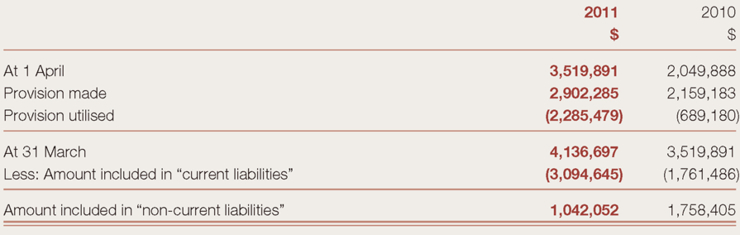

The grants are for meeting development costs of the Qualifications Framework project. 12 Receipts in advance Receipts in advance represent amounts received for programme accreditation, advice on the registration of nonlocal courses and qualifications assessment, less amounts recognised as income during the year. 13 Provision for staff gratuities

14 Reserves (a) Components of the Council’s reserves The opening and closing balances of each component of the Council’s reserves and a reconciliation between these amounts are set out in the statement of changes in reserves. (b) Nature and purpose of reserve Investment revaluation reserve The investment revaluation reserve comprises the cumulative net change in the fair value of available-for-sale securities held at the balance sheet date and is dealt with in accordance with the accounting policies in note 2(c)(iii). 15 Financial risk management and fair values and liquidity Exposure to credit and liquidity risks arises in the normal course of the Council’s operations. The Council is also exposed to equity price risk arising from its equity investments in other entities. The Council’s exposure to these risks and the financial risk management policies and practices used by the Council to manage these risks are described below. (a) Credit risk The Council’s credit risk is primarily attributable to bank deposits, accounts receivables and investments in debt securities. Management has a credit policy in place and the exposures to these credit risks are monitored on an ongoing basis. In respect of accounts receivables, individual credit evaluations are performed on all customers requiring credit over a certain amount. These take into account the customer’s past payment history, financial position and other factors. These receivables are due on presentation of billings. Normally, apart from certain customers with good credit ratings, advances are requested from customers to cover the service fee before rendering of services by the Council. The Council’s exposure to credit risk is influenced mainly by the individual characteristics of each customers. At the balance sheet date, the Council had a certain concentration of credit risk as 84% and 100% (2010: 89% and 89%) of the total accounts receivables was due from the largest customer and the four largest customers. Bank deposits are normally placed with financial institutions which have good credit ratings. Investments in debt securities are with counterparties of sound credit ratings. Given their high credit ratings, management does not expect any investment counterparty to fail to meet its obligations. The maximum exposure to credit risk is represented by the carrying amount of each financial asset in the balance sheet. The Council does not provide any other guarantees which would expose it to credit risk. Further quantitative disclosures in respect of the Council’s exposure to credit risk arising from accounts receivable are set out in note 9. (b) Liquidity risk The Council’s policy is to regularly monitor its liquidity requirements and its compliance with lending covenants, to ensure that it maintains sufficient reserves of cash and readily realisable marketable securities and adequate committed lines of funding from major financial institutions to meet its liquidity requirements in the short and long term. The earliest settlement dates of the Council’s financial liabilities at the balance sheet date are all within one year or on demand and the contractual amounts of the financial liabilities are all equal to their carrying amounts. (c) Equity price risk The Council is exposed to equity price changes arising from equity investments classified as available-for-sale equity securities (see note 8). The Council’s equity investments are blue-chip companies listed on the Stock Exchange of Hong Kong. These equity investments have been chosen based on their longer term growth potential and are monitored regularly for performance against expectations. At 31 March 2011, it is estimated that an increase/(decrease) of 10% (2010: 10%) in the market price of the Council’s available-for- sale equity securities, with all other variables held constant, would not affect the Council’s surplus or deficit unless there are impairments. The Council’s total reserves would have increased/decreased by $1,190,439 (2010: $947,844). The sensitivity analysis above indicates the instantaneous change in the Council’s surplus for the year (and accumulated surpluses) and investment revaluation reserve that would arise assuming that changes in the market value had occurred at the balance sheet date and had been applied to re-measure those financial instruments held by the Council which expose the Council to equity price risk at balance sheet date. It is also assumed that none of the Council’s available-for-sale investments would be considered impaired as a result of a decrease in the prices of respectively equity securities and that all other variables remain constant. The analysis is performed on the same basis for 2010. (d) Fair values (i) Financial instruments carried at fair value The amendments to HKFRS 7, Financial instruments: Disclosures, require disclosures relating to fair value measurements of financial instruments across three levels of a “fair value hierarchy”. The fair value of each financial instrument is categorised in its entirety based on the lowest level of input that is significant to that fair value measurement. The levels are defined as follows: – Level 1 (highest level): fair values measured using quoted prices (unadjusted) in active markets for identical financial instruments – Level 2: fair values measured using quoted prices in active markets for similar financial instruments, or using valuation techniques in which all significant inputs are directly or indirectly based on observable market data – Level 3 (lowest level): fair values measured using valuation techniques in which any significant input is not based on observable market data At 31 March 2011, the only financial instruments of the Council carried at fair value were available-for-sale equity securities of $11,904,385 (2010: $9,478,437) listed on the Stock Exchange of Hong Kong (see note 8). These instruments fall into Level 1 of the fair value hierarchy described above. During the year, there were no transfers among instruments in Level 1, Level 2 or Level 3. (ii) Fair values of financial instruments carried at other than fair value The carrying amounts of the Council’s financial instruments carried at cost or amortised cost are not materially different from their fair values at the balance sheet date. 16 Operating lease commitments At 31 March 2011, the total future minimum lease payments under non-cancellable operating leases in respect of properties are payable as follows:

The Council leases its office premises under an operating lease. The lease runs for an initial period of six years, with an option to renew the lease when all terms are renegotiated. Lease payments are usually increased periodically to reflect market rentals. The lease does not include contingent rentals. 17 Related party transactions All transactions related to the procurement of goods and services involving organisations in which a member of the Council and key management personnel may have an interest are conducted in the normal course of business and in accordance with the Council’s financial obligations and normal procurement procedures. All transactions related to the provision of accreditation services to organisations in which a member of the Council and key management personnel may have an interest are conducted in the normal course of business and in accordance with the Council’s fee charging policy and fee schedule as prescribed by the Ordinance. In addition to the transactions and balances disclosed elsewhere in these financial statements, the Council had the following related party transactions: (i) Honorarium paid to Council members in the capacity of

(ii) Key management personnel remuneration

The above remuneration is included in “staff costs” (see note 5(a)). 18 Critical accounting judgement Certain critical accounting judgement in applying the Council’s accounting policies is described below. Impairment of held-to-maturity financial assets and available-for-sale financial assets The Council follows the guidance of HKAS 39 on determining when an investment is other-than-temporarily impaired. This determination requires significant judgment. In making this judgement, the Council evaluates, among other factors, the duration and extent to which the fair value of an investment is less than its cost; and the financial health of and near-term business outlook for the investee, including factors such as industry and sector performance, changes in technology and operational and financing cash flow. 19 Possible impact of amendments, new standards and interpretations issued but not yet effective for the year ended 31 March 2011 Up to the date of issue of these financial statements, the HKICPA has issued a number of amendments, new standards and interpretations which are not yet effective for the year ended 31 March 2011 and which have not been adopted in these financial statements. The Council is in the process of making an assessment of what the impact of these amendments, new standards and new interpretations is expected to be in the period of initial application. So far it has concluded that the adoption of them is unlikely to have a significant impact on the Council’s results of operations and financial position. Analysis of expenditure for the year ended 31 March 2011 (Expressed in Hong Kong dollars)

|